Testamentary discretionary trusts: why the proposed 30% trust tax needs a rethink

On 12 May 2026, the Australian Government handed down the 2026–27 Federal Budget, which included a proposal to introduce a 30% minimum tax on discretionary trusts from 1 July 2028.

The proposal is not yet law, but it has already generated significant discussion among lawyers, accountants, advisers, and families who use trusts as part of their estate and succession planning.

Much of that discussion has focused on commonly used discretionary family trusts, income splitting, and whether wealthy Australians are using trust structures to reduce tax. That is an important policy conversation.

But it risks missing a critical point: not all discretionary trusts are the same.

In particular, testamentary discretionary trusts (often called a TDT) should not be treated as though they are simply another form of discretionary family trust. It is a different type of discretionary trust with different objectives from a discretionary family trust.

A TDT is created by a person’s will. It does not exist during the willmaker’s lifetime. It only comes into existence after the willmaker has died.

That distinction matters.

A TDT is not usually created because a person wants to move income around during their lifetime. It is created because someone has died, and their will has been carefully drafted to protect an inheritance for the people they leave behind.

Those people may be minor children. They may be a surviving spouse. They may be adult children going through financial stress, relationship breakdown, or business risk. They may be disabled or vulnerable beneficiaries. They may be grandchildren. They may be a blended family trying to preserve fairness and stability across generations.

In estate planning practice, the primary purpose of a TDT is usually asset protection, not tax minimisation.

What is a testamentary discretionary trust?

A testamentary discretionary trust (TDT) is a trust created under a person’s will.

Unlike a standard (basic) will, where an inheritance is usually given directly to a beneficiary, a TDT allows the inheritance to be held and managed through a trust structure after death. The trustee can then decide how income and capital are used for the benefit of the relevant beneficiaries, within the limits set by the will.

This flexibility can be extremely valuable.

A TDT can help protect an inheritance from being lost too early, mismanaged, or exposed to avoidable risk. It can also allow a family to adapt to circumstances that may not be known when the will is signed.

For example, a TDT may be used to:

protect young children or young adults from receiving a substantial inheritance before they are financially mature;

protect an inheritance where a surviving spouse later re-partners;

help preserve assets for children from a first relationship or blended family;

provide support for disabled or vulnerable beneficiaries;

reduce the risk of an inheritance being exposed to bankruptcy or creditor claims;

provide flexibility where a beneficiary later experiences a relationship breakdown;

support grandchildren or future generations; and

allow an inheritance to be managed responsibly over time.

These are not artificial concerns. They reflect the real complexity of modern, everyday Australian families.

Blended families are common. Relationship breakdown is common. Many adults are operating small businesses, acting as directors, or working in occupations that carry financial risk. Housing affordability is placing pressure on younger generations. Older Australians are increasingly concerned about how to protect the wealth they have built over a lifetime so that it is used for the people they intended to benefit.

In that context, TDTs are an important estate planning tool.

Why the proposed tax change matters

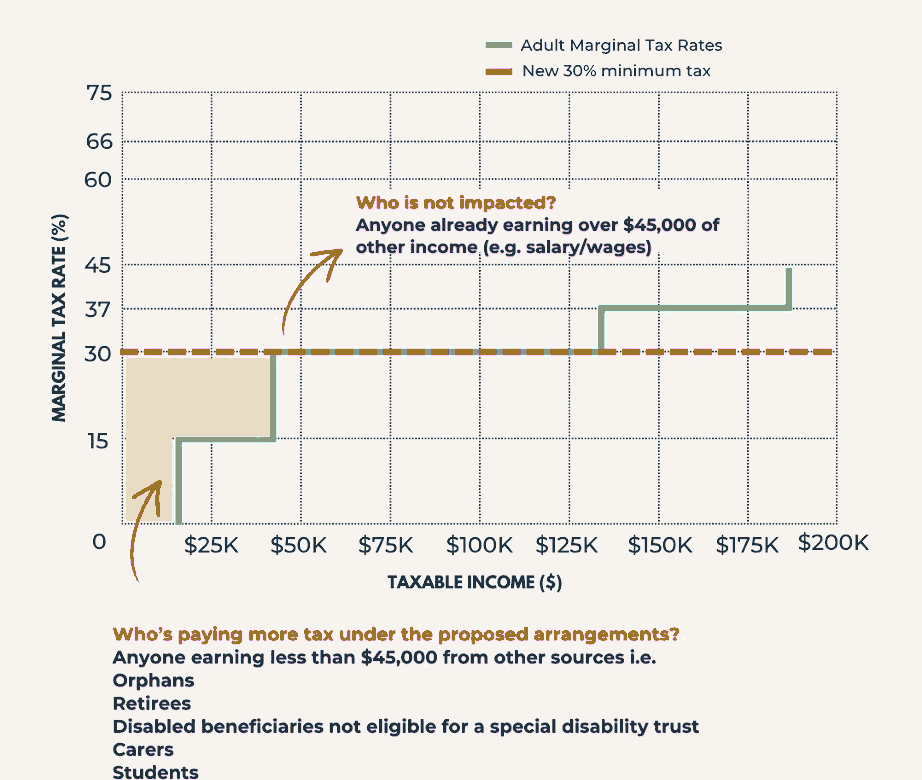

The Budget announcement indicates that the Government intends to introduce a 30% minimum tax on discretionary trusts from 1 July 2028. The tax would be paid at the trustee level, with beneficiaries, other than corporate beneficiaries, receiving non-refundable credits for tax paid by the trustee.

The stated policy concern appears to be fairness and integrity in the tax system.

However, applying the same minimum tax regime to TDTs risks producing unfair outcomes for families who are not engaged in aggressive tax planning.

For many adult beneficiaries already earning more than approximately $45,000 from salary, wages, or other income, a 30% minimum tax may not materially change the overall tax outcome. They may already be paying tax at or above that level on trust distributions.

The issue is different for lower-income beneficiaries.

A beneficiary who earns less than that amount from other sources may lose the benefit of lower marginal tax rates on income generated from their inheritance. That may include minor children, adult students, carers, widows, widowers, retirees, disabled beneficiaries, and adults who have reduced their work to care for parents, children, or grandchildren.

In other words, the proposal may have the least practical effect on higher-income earners, while creating a real cost for families who are more financially vulnerable.

That is the opposite of what good policy should do.

The 2026-27 Budget's proposed tax treatment on TDTs

Why TDTs are different from family trusts

Unlike TDTs, the much more commonly used discretionary family trust is usually established during a person’s lifetime. It may be used to operate a business, hold investments, manage family wealth, or distribute income among family members.

A TDT is different. It is created by a will. It is funded by inheritance assets. It arises only because someone has died.

This distinction is already recognised in the tax system.

Under the current tax treatment, minors who receive income from a standard family trust are generally taxed at penalty rates once the income exceeds a small threshold. This is intended to discourage artificial income splitting with children.

By contrast, income distributed to minors from a TDT is taxed at the standard adult marginal tax rates. This longstanding difference in tax treatment under a TDT recognises that the income has been generated from the investment of an inheritance (i.e., the current tax policy recognises that someone had to die to create a TDT).

A child receiving support from an inheritance is in a very different position from a child being allocated income from a family business or investment trust during their parents’ lifetime.

The current distinction is sensible. It recognises that death changes the character of estate and succession planning.

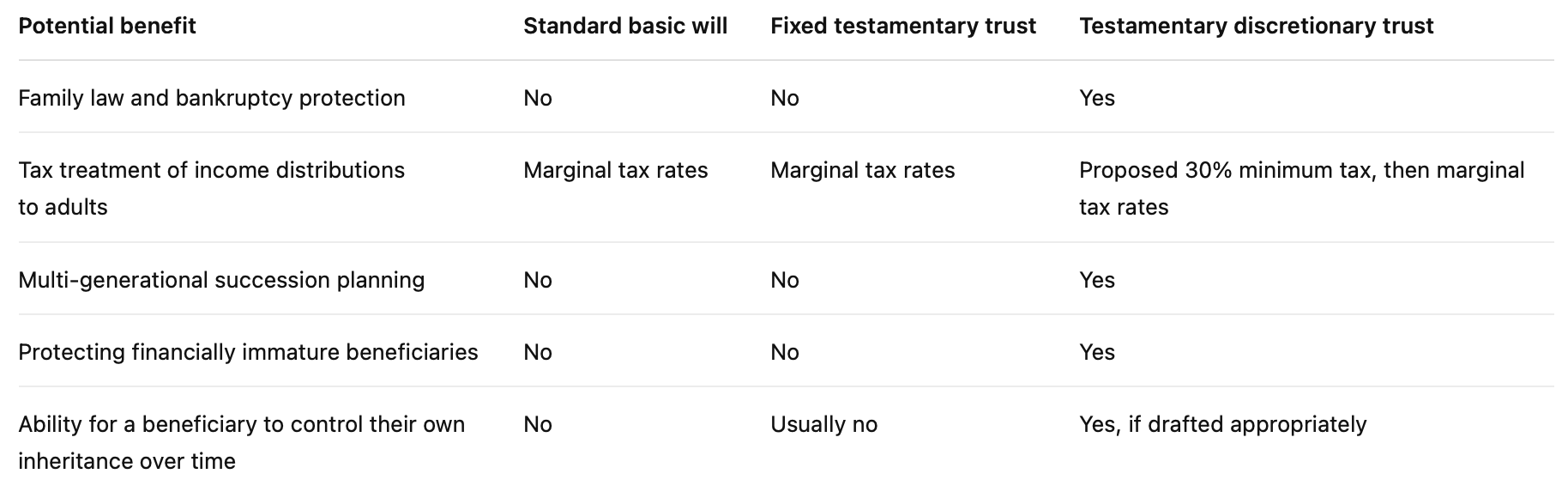

How do different estate planning structures compare

The proposed changes also raise a practical question: if TDTs become less tax effective, should families use a standard (basic) will or a fixed testamentary trust instead?

For many families, the answer will be no.

A standard (basic) will and a fixed testamentary trust may be appropriate in some circumstances. But they do not provide the same flexibility and protection as a properly drafted TDT.

Table comparing estate planning structures

A fixed testamentary trust is not an equivalent substitute for a TDT.

The whole point of a TDT is flexibility. Families do not know what the future will look like when a will is signed. A child may later experience disability, addiction, financial pressure, relationship breakdown, or bankruptcy. A surviving spouse may re-partner. A beneficiary may become vulnerable to financial exploitation. A family member may need more support than expected.

A fixed trust does not respond well to that complexity.

In many estate plans, the flexibility of a TDT is not a tax feature. It is the protection feature.

If the law encourages families to use fixed testamentary trusts instead of TDTs purely to avoid a 30% minimum tax outcome, then the law may push people into less suitable estate planning structures. That would be a poor policy outcome and a potentially devastating practical result for families.

Practical real-world examples

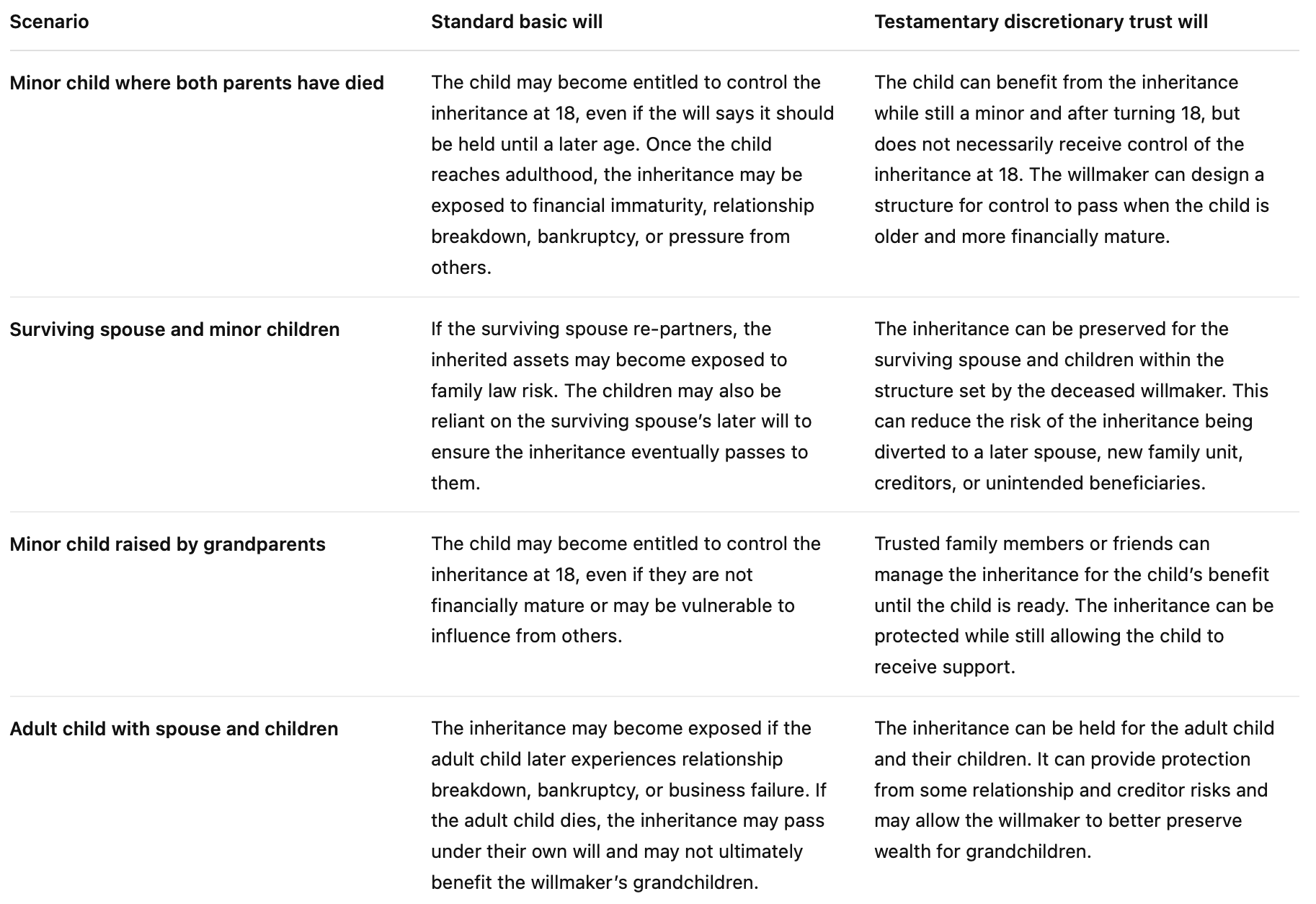

The difference between a standard (basic) will and a TDT can be significant.

The examples below are simplified, but they show why families often use TDTs for protection, flexibility, and long-term succession planning

Real-world estate planning examples

A TDT does not guarantee absolute protection in every case. No estate planning structure does. But it can materially improve the level of control, flexibility, and protection available to a family after death.

That is why many estate planning lawyers recommend TDTs for clients who want more than a standard (basic) will.

The impact on young families

One of the most concerning potential consequences is the impact on young families where one parent dies.

Consider a family where one parent dies leaving a surviving spouse and minor children. A TDT may allow income generated from the inheritance to be used flexibly for the surviving family unit. That may help pay for school costs, childcare, therapy, transport, household support, medical expenses, or other ordinary costs of raising children after a family tragedy.

This is not a luxury planning issue.

For many families, the death of a parent means the loss of income, the loss of caregiving support, or both. The surviving spouse may need to reduce their working hours. They may need to pay for additional childcare, cleaning, meal preparation, yard work, or other help to stabilise family life.

In that context, being able to allocate income from an inheritance tax-effectively for the benefit of the children can make a meaningful difference.

A tax rule designed to address high-income tax planning should not inadvertently penalise widows, widowers, and children who have lost a parent.

Grandfathering and transitional issues

The proposed start date of 1 July 2028 for the newly proposed tax regime also raises transitional questions.

If existing TDTs are to be protected, then careful thought needs to be given to wills that have already been signed and estates that are already being administered.

Estate administration often takes time. It is not unusual for an estate to take 12 months or longer to administer, especially where there are complex assets, tax issues, property sales, overseas assets, or family complications. It’s not unheard of for many estates to take 2-3 years to finalise.

There should be clear grandfathering for wills signed before the commencement date. There should also be clear protection for TDTs created by the will of a person who dies before the relevant legislative cut-off, even if the estate has not yet been fully administered and the trust has not yet been formally funded.

Families should not be left in limbo because the timing of death, administration, and legislative commencement do not align neatly.

A better policy approach

The better approach would be to exclude TDTs from the proposed 30% minimum tax regime entirely.

That would preserve the longstanding distinction between ordinary discretionary trusts created during life (like the commonly used family trusts) and TDTs created by will after death. It would also recognise that TDTs are primarily used for asset protection, family protection, and succession planning.

If the Government does not exclude all TDTs, then at a minimum, there should be targeted protections.

Those protections should include preserving ordinary marginal tax treatment for distributions to minors, disabled beneficiaries, vulnerable beneficiaries, charities, and low-income beneficiaries. Existing wills signed before commencement should also be grandfathered.

There should also be further consultation before legislation is drafted. Estate planning lawyers, tax advisers, accountants, disability advocates, family lawyers, and community organisations all have practical insight into how these structures are used in real life.

Good tax policy should address genuine integrity concerns without undermining legitimate family protection.

What should families do now?

At this stage, the proposal is not yet law.

Families should not panic, but they should pay attention.

If your will already includes a TDT, it may be worth reviewing your estate plan once further details are released. If you are preparing a new will, it is still important to consider whether a TDT is appropriate for your circumstances.

For many families, the non-tax benefits of a TDT may remain compelling even if the tax treatment changes. Asset protection, succession control, and flexibility may still justify the structure.

However, estate planning advice may need to become more tailored. The choice between a standard (basic) will, fixed testamentary trust, and a TDT will depend on the family structure, asset profile, beneficiary circumstances, tax position, and long-term objectives.

The key point is this: TDTs should not be dismissed as tax planning tools for the wealthy. They are legitimate estate planning and family succession tools that have been used for eons by everyday Australians.

Used properly, TDTs are a practical and protective estate planning structure for ordinary Australian families dealing with very human risks: death, grief, disability, relationship breakdown, financial vulnerability, and the responsibility of passing wealth safely to the next generation.

That deserves careful policy treatment.

Is your will doing enough?

A standard (basic) will may not provide the protection, flexibility, or control your family needs.

If you have children, a blended family, business interests, vulnerable beneficiaries, overseas assets, or concerns about relationship breakdown or asset protection, a TDT may still be worth considering, even if the tax rules change.

Through Life + Legacy by Latitude Legal, we help clients prepare practical, protective, and plain-English estate plans designed for modern life and business.

Book a complimentary discovery call with us to discuss a review of your estate plan and make sure your will is doing more than simply passing assets from one person to another.